It’s open enrollment season, and you know what that means: it’s time to review your health plan options and get ready for the year ahead. Whether you’re sticking with your current plan or shopping for something new, you only get the opportunity to change or adjust your plan once a year. With so many choices — from different “metal tiers” to terms like premiums, deductibles, and out-of-pocket maximums — making the right choice can feel overwhelming.

In this guide, we’ll walk you through what you can do during open enrollment, how to understand the plan tiers, and the key factors to look for when comparing coverage.

What You Can Do During Open Enrollment

Open enrollment is a period specified by your company, usually near the end of each year, when you can make changes to your health insurance plan and other benefits. Company open enrollment periods can vary in length, so pay attention to when your open enrollment period is if you get benefits through your employer.

If you’re getting individual coverage from the marketplace, the enrollment period runs from Nov 1st – Jan 15th, with Dec 15th being the cut-off date to enroll in a plan that starts Jan 1st, 2026.

During open enrollment, here’s what you can do:

- Enroll in a new health insurance plan

- Renew your current coverage

- Switch to a different plan (or tier)

- Add or remove dependents

- Update personal info like income (important for ACA subsidies)

Understanding Your Group Health Plan

When your employer offers health insurance, you may only see 1-3 plan choices during open enrollment. Plans also won’t be categorized by a metal tier. Instead, employers choose one or several healthcare plans to make available based on cost-sharing and network arrangements. A lot of the time, employer-sponsored healthcare plans are fairly generous, but make sure to look at the quality of the plan you’re being offered.

- Look beyond the premium, and check the deductible and out-of-pocket max. You could get stuck with a high bill if you actually use care.

- Check if your doctors are in-network.

- Compare prescription coverage, copays, preventive services, and specialist access.

- Consider your health needs. If your employer only offers 1 plan, but fully covers the premium, that may be the best bet — but there are other options out there for you.

If you find yourself stuck in a situation where your employer’s group plan doesn’t meet your needs, you can buy extra coverage. That usually means supplemental insurance (dental, vision, accident, critical illness coverage) rather than another full health plan. Some employers are also switching to ICHRA (Individual Coverage Health Reimbursement Arrangements) so employees can purchase the health insurance plan that makes sense for them (and covers what’s in their area.)

Benafica is an ICHRA provider for U.S. employers. Learn more about our ICHRA administration.

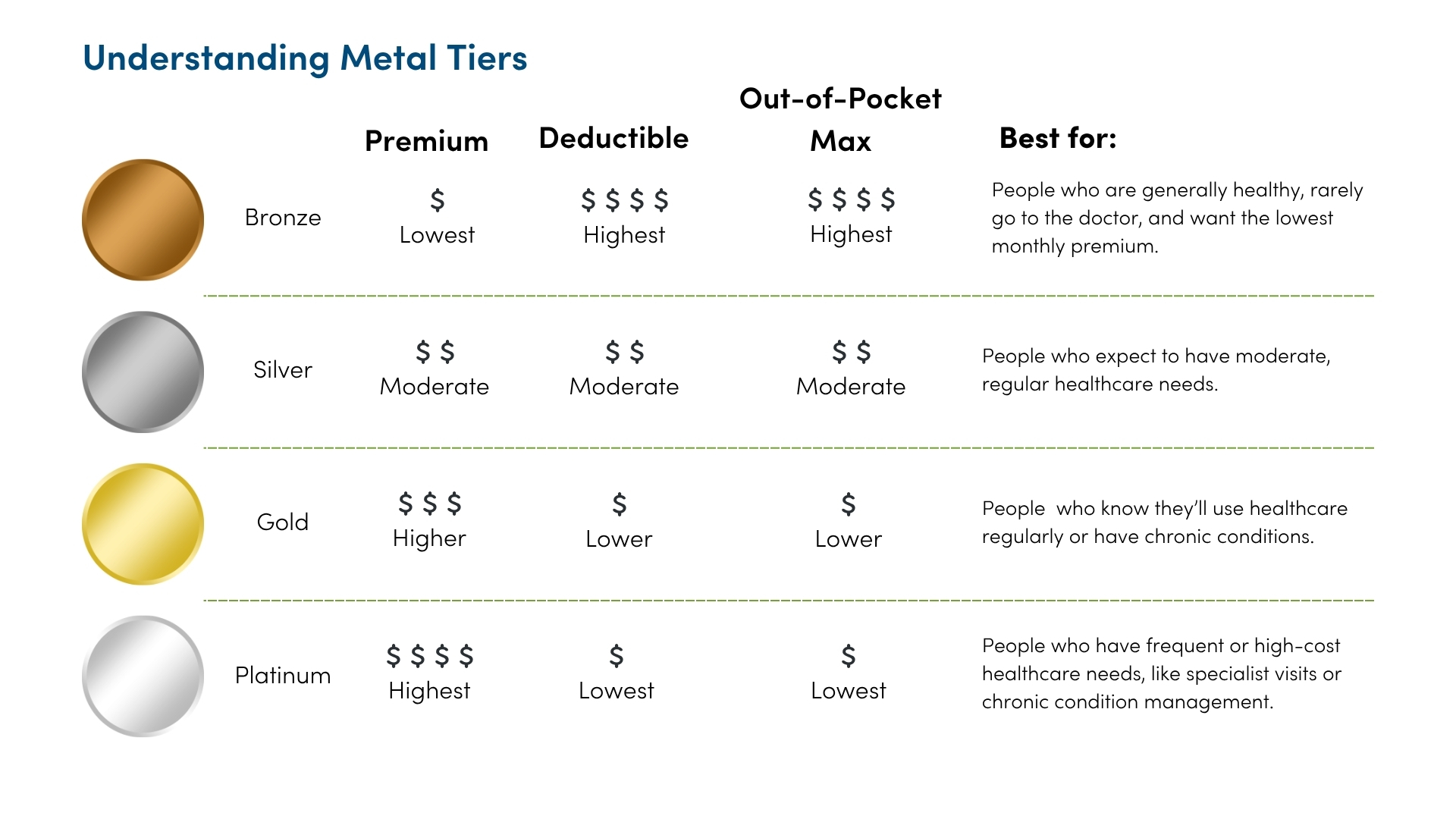

Understanding Metal Tiers

If you’re shopping for individual health insurance on the ACA Marketplace (on-exchange) or purchased directly from an insurance carrier (off-exchange), you’ll notice plans are labeled by metal tiers: Bronze, Silver, Gold and Platinum. The tiers represent the level of cost-sharing between you and the insurance company for healthcare services.

- Bronze ≈ covers 60% of costs on average, lowest monthly premium, highest out-of-pocket

- Silver ≈ 70%, balanced, subsidy-linked (cost-sharing reductions)

- Gold ≈ 80%, higher premiums, lower out-of-pocket costs

- Platinum ≈ 90%, highest premiums, lowest out-of-pocket costs

Bronze is the lowest tier with the lowest monthly premium, but the highest cost-sharing, deductible, and out-of-pocket max. If you’re a healthy person who rarely visits the doctor, a bronze plan will probably work for you (but remember if you get sick or injured, your out-of-pocket costs will be high). Platinum will be the most expensive up-front, but if you use a lot of healthcare services — like specialist visits or management of a chronic condition or illness — you’ll want to select a plan that’s going to cover the most services.

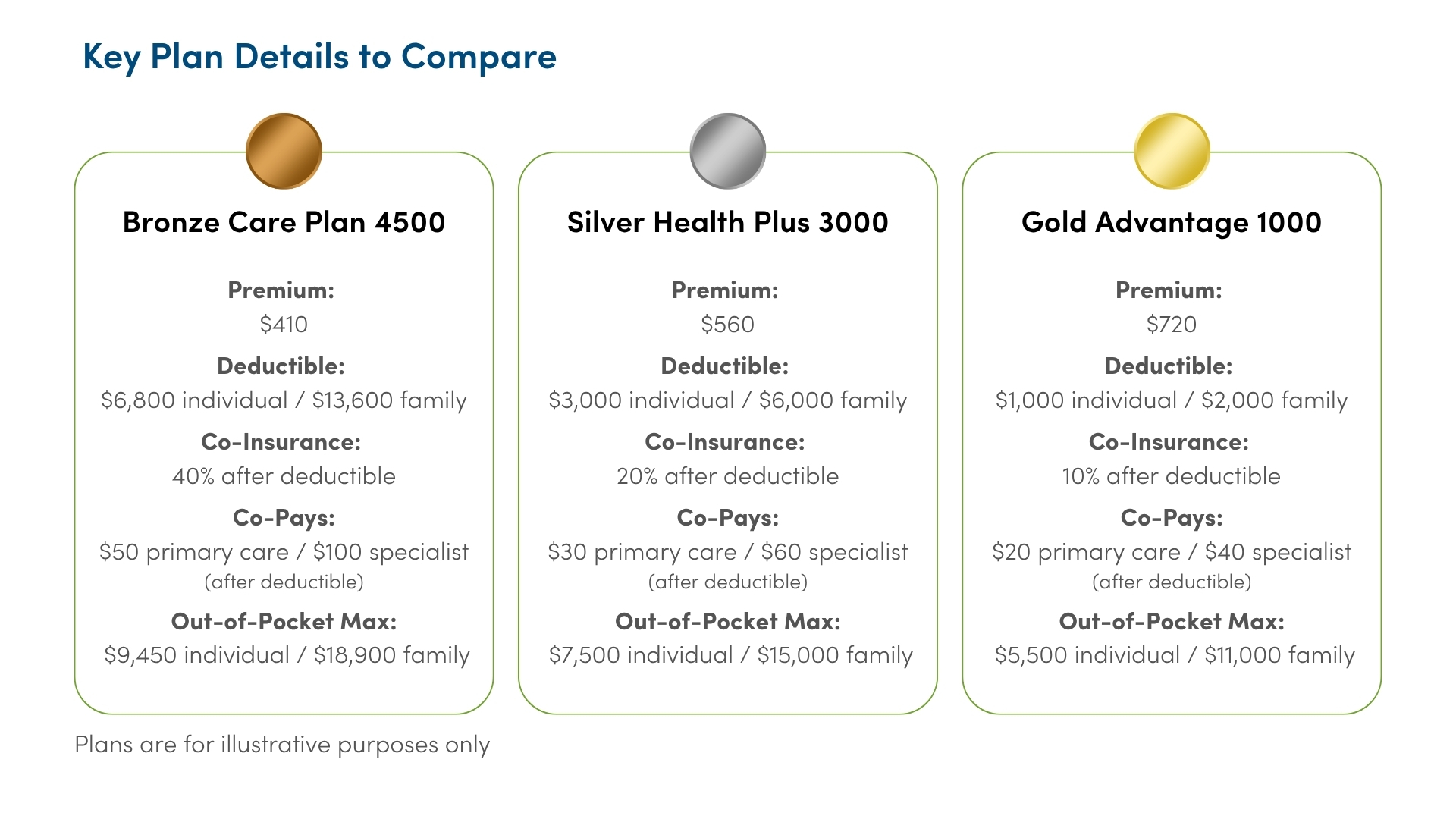

Major Plan Markers to Compare

It’s easy to get caught up in monthly premiums when choosing a health plan, because sometimes there’s only so much you can afford. But don’t ignore the bigger picture, which is the cost that comes into play when you actually start using your healthcare — deductibles, co-payments, co-insurance and out-of-pocket maximums.

- Premiums: The monthly cost you pay to keep coverage active

- Deductibles: What you pay out-of-pocket before insurance starts covering services

- Co-Payments: A fixed amount you pay towards certain services like doctor visits and specialist visits.

- Co-Insurance: The percentage of costs of a covered health care service you pay towards (20%, for example) after you’ve paid your deductible.

- Out-of-Pocket Maximums: The most you’ll pay in a year for covered services (after which insurance pays 100%)

- Individual vs. Family Maximums: The most you’ll pay in a year for just yourself or with any covered family members (if applicable)

For more information on the terminology above, read our blog on 10 Insurance Benefit Terms You Should Know

You’ll pay your premium every month, on a set date, regardless of if you go to the doctor or not.

Here’s how a deductible and co-payments work: If you go to the doctor, you might pay $30 at the front desk when you check in (co-payment) and then have a checkup and some tests that cost $425. If your deductible is $1,000, you will pay the full $425 + $30 co-pay for that visit and you would have $545 left to pay before your insurance begins helping pay for costs.

Here’s how co-insurance and out-of-pocket max works: Imagine you have an unexpected trip to the emergency room that turns into a hospital stay. Between the ER visit, surgery, and inpatient care, your bill comes to $75,000. In the weeks ahead, when the hospital bills get processed and come back, you’ll pay your full deductible of $1,000, then you’ll pay co-insurance (for example, 20% of costs) until you meet your out-of-pocket maximum at $7,500. $7,500 is the maximum you’ll pay out-of-pocket for the whole year. So any doctor’s visits that happens after this will be fully covered by the insurance company.

If you cover a spouse or children on your plan, pay attention to the family out-of-pocket max. Each person has their own limit, so one person hitting theirs doesn’t cover everyone else. The family max is usually two to three times the individual max and caps what the household pays in total. For 2025, the ACA maximum allowed OOP limit is $9,450 for an individual and $18,900 for a family. Plans can set lower amounts, but not higher.

Tips for Choosing the Right Plan

One of the biggest challenges of American health insurance is that you never know what the year ahead will bring. You might stay perfectly healthy — or face an unexpected illness or injury. That means choosing a plan often feels like a guessing game. The best approach is to base your decision on your healthcare needs from the past few years while also planning for the “what ifs.”

Look closely at provider networks and prescription coverage, and make sure you’re considering all the costs — not just premiums, but deductibles, copays, and out-of-pocket maximums. Think about your lifestyle and likelihood of needing care, whether that’s routine prescriptions, chronic condition management, or simply peace of mind for emergencies. And don’t forget: under ACA rules, preventive and wellness care is covered at no cost, no matter which plan you choose.

You don’t get a second chance at open enrollment, so plan wisely.

If you still have questions about comparing plans or navigating any of our systems, Benafica is here to help you. Individuals on a Benafica-managed ICHRA can reach out to us for help from a licensed counselor at any time.

Contact us at 651-287-3253 or support@ben360.com.